Revamp Your Golden Years with the 3 Bucket Retirement System

We all dream of a stress-free retirement, one in which we can enjoy the fruits of our years of labor without pestering money problems. However, the path to this idyllic lifestyle often confounds many, making the golden years seem more like a mirage than a possible reality. Just like how navigating through major life transitions can be emotionally draining and confusing, trying to figure out how your retirement finances will function, can be overwhelming. While there are some strategies that retirees use to create retirement income, at NewMaker Financial, we're here to help simplify the journey towards financial independence with the ‘3 Bucket System for Retirement’. It's a unique financial planning method devised to dispel the complexity around retirement planning and offers effective strategy to manage your assets.

The ‘3 Bucket System for Retirement’ is structured around three categories: short-term, long-term, and risk management. Each of these 'buckets' represent distinct horizons in your retirement income planning. The short-term bucket addresses immediate expenditure needs, the long-term bucket is set up for future growth and the risk management bucket safeguards you from unforeseen circumstances. This strategy is designed to strike a balance between being conservative to protect your savings, while still being aggressive enough to grow wealth.

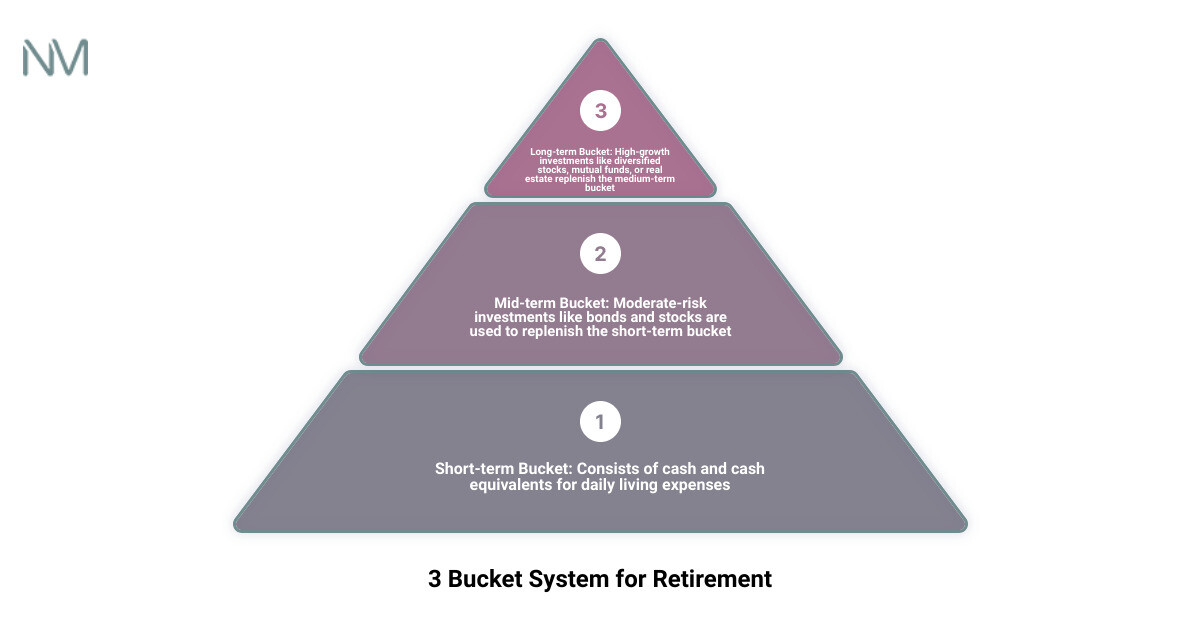

Here is a simplistic overview of the ‘3 Bucket System for Retirement':

- Short-term Bucket: Primarily consisting of cash and cash equivalents, this bucket is designed to cover your day-to-day living expenses and immediate financial needs.

- Mid-term Bucket: This bucket is set up for moderate-risk investments such as bonds and certain types of quality stocks. It mainly functions to replenish the short-term bucket when needed.

- Long-term Bucket: This bucket targets high-growth investments that may include a diversified range of stocks, mutual funds, or real estate. It is planned for more aggressive growth to replenish the medium-term bucket.

Take a look into our simple-to-understand infographic on the '3 Bucket System' to have a clear picture of how these categories interplay to keep your retirement finances healthy.

In the forthcoming sections, we will delve deeper into understanding this well-crafted system and guide you on its effective implementation. Whether you’re new to the world of financial planning or seeking a way to streamline your existing retirement plan, the '3 Bucket System for Retirement' offers a comprehensive and yet, appealing approach to manage your golden years better.

Understanding the 3 Bucket Retirement System

Retirement doesn't have to feel like stepping off a financial cliff. With the right strategy, you get to glide down smoothly, enjoying the view as you descend. At the heart of the 3 bucket retirement system is a simple yet powerful concept: divide and conquer. You divide your retirement savings into three categories or "buckets," each with its specific purpose, risk level, and investment strategy. This allows you to manage your assets effectively and ensure a secure income stream during your retirement.

The Concept of the 3 Bucket Retirement System

The 3 bucket retirement system is, at its core, an income strategy that uses time-segmented "mini" portfolios to designate the right level of risk-to-reward ratio with the appropriate future timeframe. In simpler terms, your retirement savings will be split into three main segments: short-term, intermediate, and long-term. The idea is to match your assets with your income needs over time.

The short-term bucket covers your immediate income needs. It's filled with safe, low-risk assets that provide a stable income, shielding you from the immediate impact of market volatility.

The intermediate bucket is your buffer. It's designed to generate income and stability for the medium term (three to seven years ahead). It carries a moderate risk level, balancing safety with growth.

The long-term bucket is your growth engine. It's aimed at high-risk investments that help you beat inflation over the long haul. This bucket is all about securing your financial future, providing you with income for a decade and beyond.

The Three Categories: Short-term, Long-term, and Risk Management

Each bucket in this system serves a specific purpose and follows a distinct investment strategy. The short-term bucket focuses on liquidity, ensuring that you can meet your income needs without worrying about market fluctuations. Assets in this bucket include cash, money market funds, and short-term bonds.

The long-term bucket, on the other hand, is dedicated to growth. It includes high-risk investments like individual stocks, real estate, cryptocurrency, and more. The goal is to provide meaningful returns over the next decade and beyond, helping you beat inflation.

Risk management is a crucial aspect of this system. It involves regularly reviewing and rebalancing your buckets to ensure they stay aligned with your income needs and risk tolerance. As your circumstances change, so does the composition of your buckets.

The Role of the 3 Bucket System in Building Wealth

The 3 bucket system is more than just a retirement strategy. It's a comprehensive approach to building wealth. By dividing your assets into distinct buckets, you can optimize your investments based on your income needs, time horizon, and risk tolerance.

You'll have a consistent income stream to cover your spending needs, thanks to your short-term bucket. Your intermediate bucket will provide stability and income for the medium term. And your long-term bucket will fuel your wealth growth, ensuring that you have enough resources for your later retirement years.

At NewMaker Financial, we're committed to helping you navigate your financial journey. Whether you're just starting your retirement planning or looking to refine your strategy, the 3 bucket system can offer the structure, flexibility, and peace of mind you need to secure your golden years. It's time to take control of your financial future, one bucket at a time.

Implementing the 3 Bucket Retirement System

Feeling the thrill of taking control of your retirement finances yet? Fantastic! Now let's dive into the details of setting up your 3 bucket retirement system. It's time to fill those buckets up!

Setting Up the Short-term Bucket: Cash and Cash Equivalents

The first bucket is your short-term bucket, and it holds your immediate expenses for the next one to two years. This includes living expenses and any upcoming major expenses. Picture it as your personal financial buffer against the ebb and flow of market fluctuations.

The key is to fill this bucket with cash and cash equivalents, which are low-risk and highly liquid assets. Remember, the main goal of this bucket is liquidity, not high yield. The assets in this bucket are not intended to generate significant returns, but they provide the reliability you need for your day-to-day expenses. They should allow you to meet your income needs without worrying about the market's current state.

Building the Mid-term Bucket: Low-risk Investments

Next, we have the intermediate bucket. Think of this bucket as your financial bridge between the short-term and long-term buckets. This bucket is designed to generate income and stability for expenses anticipated three to seven years from now.

The risk level in this bucket is medium. You're not playing it too safe to the point that you can't keep pace with inflation, but you're also not being too risky that potential losses could compromise your ability to meet your income needs. Ideal assets to fill this bucket include longer-term bonds, CDs, real estate investment trusts, and preferred stocks.

Creating the Long-term Bucket: High-risk Investments for Growth

Finally, we have the long-term bucket. This is your growth engine, designed to beat inflation over the long haul. Assets in this bucket are high-risk investments expected to yield substantial returns over the next decade and beyond.

These might include individual stocks, real estate, cryptocurrency, private equity funds, hedge funds, IPO investing, and venture capital investing. While these investments may fluctuate in the short term, the goal is to net meaningful returns over the long term.

As these investments generate income, you can use it to top off your intermediate bucket, creating a cycle that keeps your retirement finances flowing smoothly.

Remember, implementing the 3 bucket retirement system requires careful planning and regular review. At NewMaker Financial, we stand ready to guide you through the process, ensuring your buckets are well-balanced and aligned with your retirement goals.

Advantages and Disadvantages of the 3 Bucket Retirement System

As we delve deeper into the 3 Bucket Retirement System, it's essential to reveal both the system's strengths and potential weaknesses. While this financial strategy offers significant advantages, no single approach is perfect. Let's explore the benefits and drawbacks, helping you make an informed decision about whether this is the right strategy for your retirement.

Benefits of the 3 Bucket Retirement System

The 3 Bucket retirement strategy offers multiple benefits that can help ensure a comfortable and worry-free retirement:

- Asset diversification: This strategy inherently promotes asset diversification. With your money in three different 'buckets' based on your needs and time horizons, you're spreading your risk across various investment types.

- Flexibility: The 3 Bucket system provides a degree of flexibility that allows you to adjust your investments according to life changes or market fluctuations.

- Income security: With a bucket dedicated to short-term needs, you can have peace of mind knowing that your immediate income needs are covered.

- Growth potential: The long-term bucket, being more aggressive and growth-oriented, offers the potential for higher returns over a longer period.

- Inflation protection: By dividing your assets among cash, low-risk, and high-risk investments, you create a buffer against the eroding effects of inflation.

Drawbacks of the 3 Bucket Retirement System

Despite its many advantages, the 3 Bucket Retirement System also has potential limitations:

- Sufficient assets required: To effectively fund each bucket, you need a significant amount of assets. If your retirement fund is stretched thin, you might find it difficult to adequately fund each bucket.

- May not align with your investment style: Every investor has a unique style and risk tolerance. Some might prefer to invest more in high-risk stocks or play it extra safe. The 3 Bucket strategy might require more work to reflect your investment preferences.

- Requires active management and rebalancing: The bucket strategy gives a roadmap for retirement income, but the actual assets you choose for each bucket are entirely up to you. Regular rebalancing of your portfolio is needed to keep your buckets aligned.

In conclusion, the 3 Bucket Retirement System offers a comprehensive approach to managing your retirement finances. However, it requires careful planning, sufficient assets, and active management. At NewMaker Financial, we can help you navigate these challenges and implement a 3 Bucket Retirement System tailored to your unique needs and goals.

The 3 Bucket Retirement System and the Financial Order of Operations

In the world of financial planning, the 3 Bucket Retirement System is a powerful tool. But to truly harness its potential, it's crucial to understand how it fits into the larger Financial Order of Operations. Let's explore this interplay and discover how you can build wealth step-by-step using this system and keep track of your progress.

Step-by-step Guide to Building Wealth with the 3 Bucket System

The beauty of the 3 Bucket Retirement System lies in its simplicity. It begins with the creation of three "buckets" or portfolios, each serving a distinct purpose.

-

Short-term Bucket: This bucket contains cash and cash equivalents, such as money market funds or short-term bonds. It's meant to cover immediate expenses and has an investment horizon of up to two years. It's designed to be low risk and easily accessible.

-

Mid-term Bucket: This bucket consists of low-risk investments like bonds or fixed-income securities. It aims to provide income over the medium term (3 to 10 years) and is moderately risk-tolerant.

-

Long-term Bucket: This bucket, meant for growth, is more aggressive and includes high-risk investments like stocks. It has a long-term investment horizon of over ten years.

By strategically allocating your assets across these three buckets, you can balance your need for immediate income, growth potential, and risk management. The key is to regularly replenish the short-term bucket using the returns from the other two buckets, a practice we at NewMaker Financial refer to as "buy low, sell high" principle.

Tracking Progress: The Importance of an Annual Net Worth Statement

Implementing the 3 Bucket System is just the beginning. To truly revamp your golden years, it's critical to track your progress regularly. One of the most effective ways to do this is by maintaining an annual net worth statement.

An annual net worth statement provides a snapshot of your financial health. It details your assets (including all three buckets) and liabilities, helping you understand your overall financial position. By comparing these statements year after year, you can gauge how well your 3 Bucket System is performing and make necessary adjustments.

Remember, financial planning is not a one-size-fits-all process. It requires constant monitoring and tweaking to ensure it aligns with your changing needs and market conditions. At NewMaker Financial, we can guide you through this process, helping you optimize the 3 Bucket Retirement System for your unique situation.

In the end, the 3 Bucket Retirement System is more than just a strategy; it's a roadmap to financial independence. By understanding its role in the Financial Order of Operations and tracking your progress, you can navigate the complexities of retirement planning and enjoy a financially secure future. After all, isn't that the golden dream?

Personalizing the 3 Bucket Retirement System

As we transition into the last phase of our retirement planning guide, let's delve into how to personalize the 3 Bucket Retirement System. Remember, the beauty of this strategy is its flexibility. It can be tailored to fit your unique financial landscape, factoring in your risk tolerance, the ever-present inflation, and the unpredictable nature of market fluctuations.

Considering Individual Risk Tolerance, Inflation, and Market Fluctuations

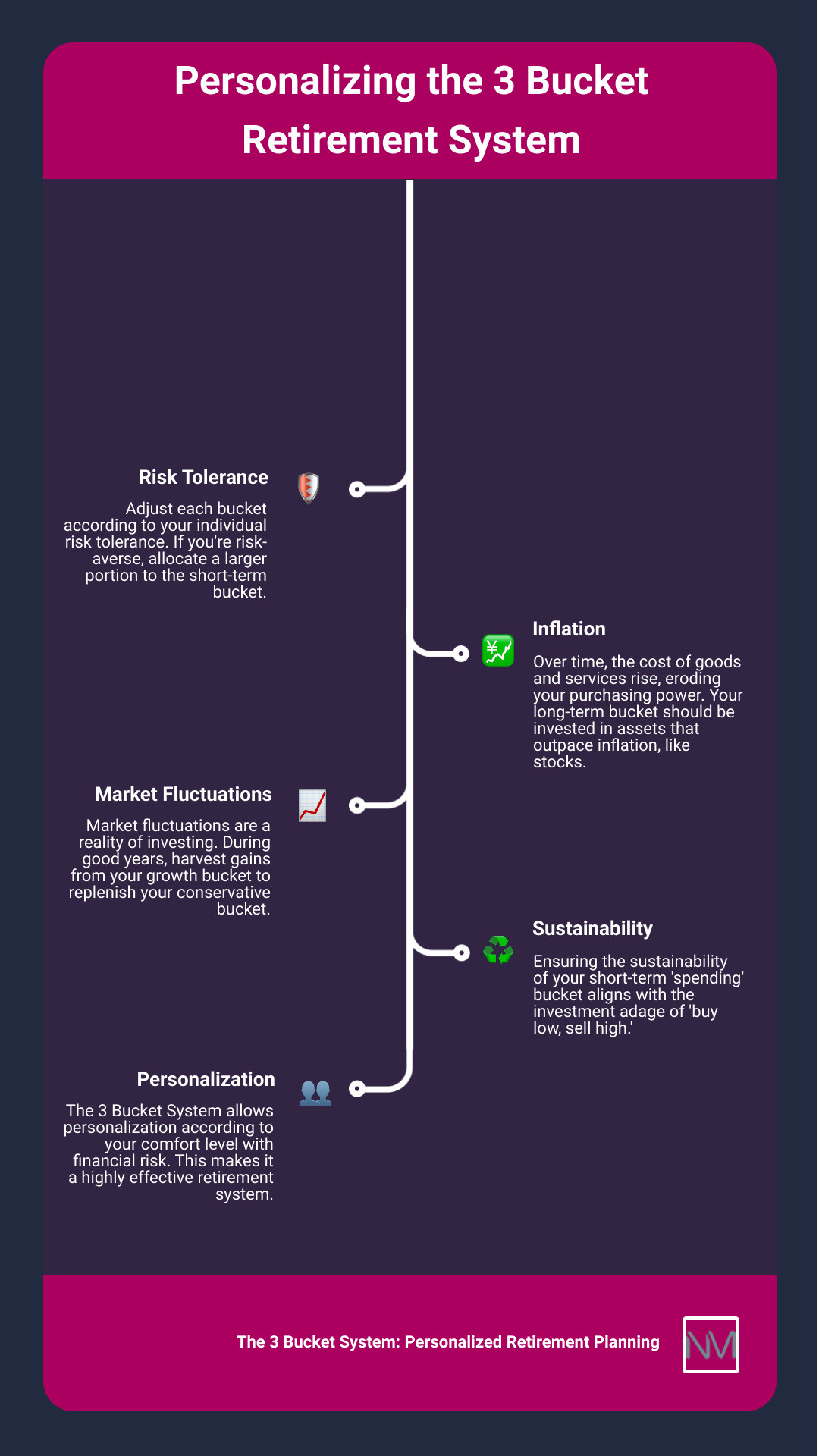

Every person has a different level of comfort when it comes to financial risk. This is why the 3 Bucket System is so effective; it allows you to adjust each bucket according to your individual risk tolerance. If you're more risk-averse, you might choose to allocate a larger portion of your assets to the short-term bucket, which should be the most conservative. If you're comfortable with higher risk for potentially higher returns, you might put more into the long-term bucket, which is more growth-oriented.

Inflation is another factor to consider. Over time, the cost of goods and services tends to rise, which can erode your purchasing power. To combat this, your long-term bucket should be invested in assets that have the potential to outpace inflation, such as stocks.

Market fluctuations are a reality of investing. During good years, we suggest harvesting gains from your growth bucket to replenish your conservative bucket. This practice not only ensures the sustainability of your short-term "spending" bucket but also aligns with the age-old investment adage of "buy low, sell high."

The Role of a Financial Planner in Implementing the 3 Bucket System

While understanding and setting up the 3 Bucket Retirement System is a critical first step, ongoing management is just as important. This is where a financial planner at NewMaker Financial can help. As your financial guide, we will work closely with you to keep your buckets balanced, adjusting the allocations as needed based on your changing needs, market conditions, and other key financial indicators.

We will also help you navigate major life transitions, such as a divorce or the loss of a loved one, which can significantly impact your financial situation. With our expert advice, you can make prudent financial decisions during these challenging times, ensuring your retirement planning stays on track.

At NewMaker Financial, we aim to alleviate stress and provide guidance through life's ups and downs, helping you stay on a path towards financial stability. So, whether you're just starting your retirement planning journey or looking to tweak your existing strategy, our team is here to help you implement and optimize your 3 Bucket Retirement System.

Remember, your golden years should be about enjoying the fruits of your hard work, not worrying about finances. And with the 3 Bucket Retirement System, you can create a personalized financial plan that aligns with your vision of a dream retirement.

Conclusion: Revamping Your Retirement with the 3 Bucket System

As we wrap up our deep dive into the 3 Bucket Retirement System, it's clear that this innovative method of financial planning can offer a solid framework for those transitioning into their golden years. Whether you're dealing with a major life change or simply looking to secure a stable financial future, implementing this strategy can transform the way you approach retirement planning.

At NewMaker Financial, we believe that everyone deserves the peace of mind that comes with knowing their retirement is secure. Our goal is to empower you to take control of your financial future, one bucket at a time.

By dividing your assets into short-term, mid-term, and long-term buckets, you can fine-tune your investment decisions based on your retirement timeline and risk tolerance. This approach not only provides a steady income stream for your retirement years but also helps to protect your nest egg from potential market fluctuations.

However, it's essential to remember that the 3 Bucket Retirement System isn't a one-size-fits-all solution. Personalizing this system based on your unique needs and circumstances is crucial to its success. Whether you're considering your risk tolerance, inflation, or market fluctuations, tailoring the 3 Bucket System to your situation will ensure it works efficiently for you.

In this journey, the role of a financial planner can be instrumental. Their expert guidance can help you navigate the complexities of the financial world and make informed decisions about your retirement planning. At NewMaker Financial, we're committed to providing you with the tools and advice you need to make your retirement dreams a reality.

Revamping your retirement with the 3 Bucket System is more than just a financial strategy; it's about paving the way for a worry-free and fulfilling retirement. After all, you've worked hard throughout your life, and it's time to enjoy the fruit of your labor.

As we always say at NewMaker Financial, your golden years should be golden in every sense. So why not start today? Take the first step towards a secure and enjoyable retirement by implementing the 3 Bucket Retirement System. And remember, we're here to guide you every step of the way.

In the end, your retirement should be a time of relaxation and enjoyment, not financial stress. The 3 Bucket Retirement System can be the key to unlocking the retirement lifestyle you've always dreamed of. So why wait? Revamp your retirement today, and look forward to a brighter, more secure tomorrow.